稳定币是一种加密货币,其市场价值与另一种货币、商品或金融工具挂钩。对于那些在加密货币行业活跃的人来说,您无疑意识到加密资产的高波动性。尽管它们可能助长投机,但这可能会阻碍现实世界的采用。通过稳定币,投资者可以用与传统市场挂钩的交换媒介来缓和风险暴露。这些资产为日常交易提供了一种“稳定”的货币。

如今,稳定币市场的价值约为1500亿美元,并且正在快速增长。然而,随着巨大的增长,失败的风险也随之而来。广泛使用的稳定币项目的崩溃对加密空间产生了重大影响。在2022年熊市期间,Terra的UST崩溃导致了整个加密货币行业的传染效应。USDT的快速增长及其随之而来的批评引起了监管机构的更多关注,尤其是因为稳定币的失败对更广泛的金融系统产生了重大影响。

什么使稳定币稳定?

简单来说,稳定币通过算法公式或保持储备资产作为抵押来保持与资产价值的挂钩。稳定币主要有三种类型:

法币抵押稳定币:

这些稳定币由现实世界资产的储备支持,例如美元、欧元或黄金。这些资产存放在银行或其他金融机构中,可以以1:1的比例兑换现金。法币抵押稳定币的例子包括Tether (USDT)、USD Coin (USDC)和Paxos Standard (PAX)。

加密货币抵押稳定币:

这些稳定币由加密货币资产的储备支持,例如比特币或以太坊。这些资产存放在区块链上的智能合约中,可以按抵押品的价值兑换稳定币。加密货币抵押稳定币的例子包括DAI和sUSD。

非抵押稳定币:

这些稳定币不由任何实物资产或储备支持。相反,它们依赖复杂的数学算法来控制稳定币的供应,以保持其价值稳定。非抵押稳定币的例子包括Ampleforth (AMPL)和Basis (BAS)。

法币抵押稳定币

最简单理解的稳定币是那些可以兑换为其挂钩的外部参考的稳定币。也就是说,这些稳定币是以法币1:1抵押的。例如,一个与1美元挂钩的法币抵押稳定币可以兑换为1美元法币。这更像是美元的数字表示,而不是挂钩,它需要一个集中保管人来持有储备。您不仅需要信任这个保管人,还需要信任审计师确保保管人使用最佳实践来维持适当的储备。如果负责储备的集中实体确实维持适当的抵押品,那么法币抵押稳定币可以承受任何程度的加密货币波动。

好处

- 通过法币储备实现1:1的价格稳定。

- 简单的机制使其易于理解。

- 抵押品存放在区块链之外,因此该系统不易受到黑客攻击。

缺点

- 与DeFi的采用相悖 - 它需要一个可信的保管人来管理法币储备(集中化)。

- 转换为法币的成本高且速度慢。

- 需要定期审计以保持透明度并确保法币储备得到维护。

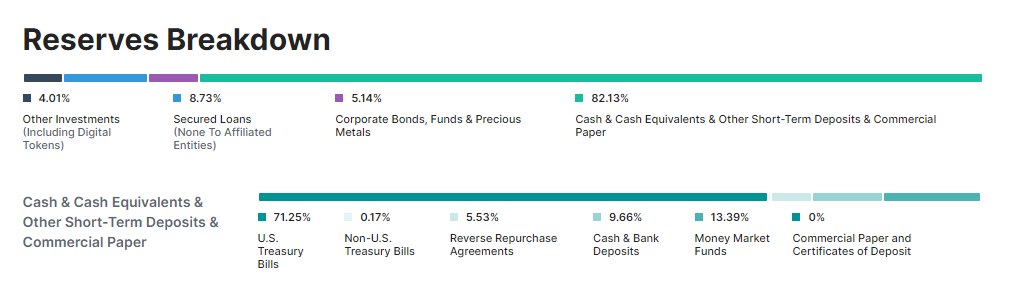

Tether的USDT是市值最大的稳定币(在稳定币中),是一个由储备支持的稳定币的例子。在2014年至2017年间,Tether宣传USDT是100%由法币储备支持的,并且可以随时以1:1的比例兑换美元。然而,自2017年以来,Tether卷入了争议。2019年,Tether承认他们的储备并不是由法币支持的,而是由“传统货币、现金等价物和Tether向第三方提供的贷款的其他资产和应收款的混合。”

自那时以来,Tether已披露只有约8%的储备实际上是以现金形式持有的。Tether在其财务审计方面也一直存在持续的延迟,最终在2022年12月完成。Tether储备的当前分解在下面的图形中突出显示:

不幸的是,信任集中实体的需要维持了现状,并将加密行业束缚在它试图摆脱的事物上:传统金融。

按市值计算的下两个最大的法币抵押稳定币是USDC和BUSD。它们的储备主要包含美国国债和一些法币(<25%),并且他们宣传希望对其抵押品保持透明。

加密货币抵押稳定币

如果一个加密项目致力于DeFi,那么该项目的创始人自然会希望避免法币系统和集中化。要拥有一个完全远离法币的稳定币(但仍依赖于储备的概念),可以使用另一种加密货币作为储备。这个模型的问题在于,加密货币的价格波动,因此储存在储备中的抵押品的价值可能会受到类似的波动。确保储备足以抵御储备加密货币的巨大下跌价格行动的唯一方法是过度抵押稳定币,以便它可以吸收抵押品的重大价格波动。

一个加密货币抵押稳定币的例子是DAI,它由Ethereum上的makerDAO项目发行。DAI与美元挂钩,其价值通过抵押债务头寸(CDPs)维持。

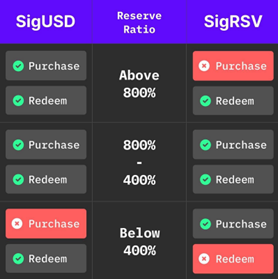

SigmaUSD是一个去中心化的稳定币发行协议的例子,它使用储备并且不由债务头寸抵押。

每个人都可以铸造SigUSD以及SigRSV(为平台提供储备)。该协议允许人们持有由Ergo支持的美元,并通过锁定他们的ERG作为储备资本来赚取佣金费用。基于储备的模型优于使用抵押债务头寸,因为它能够在抵押资产的极端波动期间防止级联清算。

该协议使用400%到800%之间的储备比率,为买家、卖家和持有者创造健康的流动性。储备比率是流通中的SigUSD的价值与储存在储备中的ERG的价值之间的比率。因此,如果流通中有1000个SigUSD,而储备中存储的1000个ERG的价值为5美元,则储备比率为500%。

您可能会想,保持储备比率在400%到800%之间意味着什么?如果储备比率低于400%,则合同会阻止用户将SigRSV兑换为储备中存储的ERG。通过这样做,协议可以维持美元和SigUSD的平价。此外,当储备比率低于400%时,用户将无法铸造SigUSD。如果ERG的价值上升并使储备比率超过400%,则可以发行更多的SigUSD。同样,如果ERG的价值下降并且储备比率低于400%,则SigUSD的铸造将被锁定。

这意味着如果某人铸造价值100美元的SigUSD,则将有价值400美元的SigRSV支持它。这使其等同于75%的抵押债务头寸。该系统保护SigUSD与美元的挂钩,并防止在储备比率低于400%时发生闪崩。

SigRSV的持有者从协议的交易中受益。铸造或兑换SigUSD的用户支付2.25%的费用,这些费用将归储备持有者所有。

非抵押稳定币

非抵押稳定币也被称为算法、铸币风格稳定币或未来增长支持的稳定币。这些稳定币不依赖抵押资产来维持其价值,而是使用数学算法来控制稳定币的供应,以保持其价值稳定。Dexy是一个铸币风格稳定币的例子。

Dexy协议使用ERG作为储备,Dexy作为稳定币。它有两个一起运作的合同:一个银行和一个DEX(CP-AMM)。银行持有储备以供部署,并在DEX中铸造新的Dexy。DEX试图维持一个预言机价格,并具有买入和卖出功能。

使用Dexy框架构建的第一个产品是DexyGold,其中稳定币的价格与USD/XAU v2 预言机池挂钩。Dexy使用单向绑定机制,其中Dexy代币是根据预言机池的汇率从发行合同中铸造的,并可以在流动性池(LP)上出售,类似于Uniswap V2。为了确保协议的稳定性,当预言机池的汇率低于LP汇率的某个百分比时,不允许赎回LP代币。

如果预言机池的汇率高于LP汇率,则交易者可以通过从发行箱中铸造Dexy代币并将其出售给LP来进行套利。如果预言机池的汇率低于LP汇率,则可以使用在发行箱中收集的ERG通过进行交换来将汇率拉回。

超越稳定币:点对点货币

ChainCash是一个去中心化的点对点货币系统,旨在通过信任和区块链资产共同创造货币。它解决了区块链资产供应的非弹性问题,这可能会阻碍它们在现实世界中的使用。Chaincash允许以去中心化的方式弹性创建货币,同时保持货币的质量。

ChainCash的用户可以创建任意价值的票据,这些票据可能由各种数字代币或现实世界资产的储备支持,也可能不支持。这些票据就像货币的数字表示,可以在ChainCash系统内用于交易。为了保持货币的质量,票据的接受取决于对发行者的抵押或信任。随着票据的流通,由于集体抵押和信任的支持,它们的质量通常会提高。

ChainCash的实施将使用两个合同:一个用于票据,一个用于储备。该系统可以跟踪不同的票据和储备合同,支持各种接受谓词和赎回机制,并容纳互补货币系统,例如地方交换交易系统(LETS)和地方货币。

虽然第二层实施仍在考虑中,但ChainCash提供了一个灵活且去中心化的货币系统,具有满足全球不同经济主体的潜力,解决传统区块链资产的局限性。

结论

稳定币是加密货币行业的重要组成部分,因为它们充当桥梁,将传统金融与基于区块链的新加密系统整合在一起。尽管SigUSD协议取得了巨大的成功,但Ergo上的开发者们继续创新加密稳定币的潜在设计。目前,正在开发两个主要的金融框架:Dexy和ChainCash。随着跨链桥(如Rosenbridge)的发展,Ergo的稳定币有潜力为许多其他区块链用户提供安全和稳定的价值储存 - 这是行业迫切需要的。

Share post