Stablecoin: Cosa Sono e Come Funzionano?

4 maggio 2023

Le stablecoin sono un tipo di criptovaluta il cui valore di mercato è ancorato a un'altra valuta, merce o strumento finanziario. Per coloro che sono stati attivi nell'industria delle criptovalute, non c'è dubbio che siate a conoscenza dell'alta volatilità degli asset crittografici. Sebbene possano alimentare la speculazione, ciò può ostacolare l'adozione nel mondo reale. Con le stablecoin, gli investitori possono temperare la loro esposizione al rischio con un mezzo di scambio ancorato ai mercati tradizionali. Questi asset forniscono una valuta 'stabile' per le transazioni quotidiane.

Oggi, il mercato delle stablecoin vale circa 150 miliardi di dollari ed è in rapida crescita. Tuttavia, con una crescita massiccia arriva il rischio di fallimento. I crolli di progetti di stablecoin ampiamente utilizzati hanno avuto conseguenze significative per lo spazio crittografico. Con il crollo dell'UST di Terra durante il mercato orso del 2022, il contagio ha avuto un effetto domino su tutta l'industria delle criptovalute. La rapida crescita e le critiche successive di USDT hanno attirato un'attenzione crescente da parte dei regolatori, soprattutto poiché i fallimenti delle stablecoin hanno avuto un impatto significativo sui sistemi finanziari più ampi.

Cosa Rende una Stablecoin Stabile?

In parole semplici, le stablecoin rimangono ancorate al valore di un asset attraverso formule algoritmiche o mantenendo asset di riserva come garanzia. Ci sono tre principali tipi di stablecoin:

Stablecoin collateralizzate in fiat:

Queste stablecoin sono supportate da una riserva di asset del mondo reale, come dollari statunitensi, euro o oro. Questi asset sono detenuti in una banca o in un'altra istituzione finanziaria e possono essere riscattati per contante a un tasso di 1:1. Esempi di stablecoin collateralizzate in fiat includono Tether (USDT), USD Coin (USDC) e Paxos Standard (PAX).

Stablecoin collateralizzate in criptovaluta:

Queste stablecoin sono supportate da una riserva di asset crittografici, come Bitcoin o Ethereum. Questi asset sono detenuti in un contratto intelligente su una blockchain e possono essere riscattati per la stablecoin a un tasso determinato dal valore della garanzia. Esempi di stablecoin collateralizzate in criptovaluta includono DAI e sUSD.

Stablecoin non collateralizzate:

Queste stablecoin non sono supportate da alcun asset fisico o riserva. Invece, si basano su complessi algoritmi matematici per controllare l'offerta della stablecoin al fine di mantenere il suo valore stabile. Esempi di stablecoin non collateralizzate includono Ampleforth (AMPL) e Basis (BAS).

Stablecoin Collateralizzate in Fiat

Il tipo più semplice di stablecoin da comprendere è quello che è riscattabile per il riferimento esterno a cui è ancorato. Cioè, queste stablecoin sono collateralizzate 1:1 in fiat. Ad esempio, una stablecoin collateralizzata in fiat ancorata a 1 USD può essere riscattata per 1 USD fiat. Questo è meno un'ancora e più una rappresentazione digitale di un dollaro, dove richiede un custode centralizzato per detenere la riserva. Non solo devi fidarti di questo custode, ma devi anche fidarti che i revisori garantiscano che il custode stia utilizzando le migliori pratiche per mantenere le riserve appropriate. Se le entità centralizzate responsabili della riserva mantengono davvero il collaterale appropriato, allora le stablecoin collateralizzate in fiat possono resistere a qualsiasi quantità di volatilità delle criptovalute.

Vantaggi

- Stabilità del prezzo 1:1 attraverso riserve fiat.

- Meccanismo semplice che lo rende facile da comprendere.

- Il collaterale è detenuto al di fuori della blockchain, quindi questo sistema è meno vulnerabile agli attacchi.

Svantaggi

- Antitetico all'adozione di DeFi - richiede un custode fidato per gestire una riserva fiat (centralizzata).

- Costoso e lento da liquidare in fiat.

- Richiede audit regolari per mantenere la trasparenza e garantire che le riserve fiat siano mantenute.

L'USDT di Tether è una stablecoin con la maggiore capitalizzazione di mercato (tra le stablecoin) ed è un esempio di una stablecoin supportata da una riserva. Tra il 2014 e il 2017, Tether ha promosso che l'USDT era supportato al 100% da riserve fiat e poteva essere scambiato 1:1 per USD in qualsiasi momento. Tuttavia, dal 2017, Tether è stata coinvolta in controversie. Nel 2019, Tether ha ammesso che le loro riserve non erano supportate da fiat, ma erano invece un mix di “valuta tradizionale, equivalenti di cassa, [e] altri asset e crediti da prestiti effettuati da Tether a terzi, che possono includere parti affiliate.”

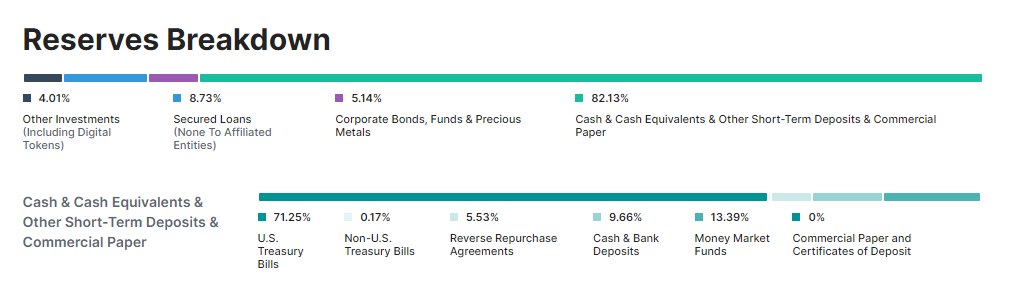

Da allora, Tether ha divulgato che solo ≅8% delle riserve erano effettivamente detenute in contante. Tether ha anche avuto ritardi costanti quando si tratta degli audit delle sue finanze, che sono stati finalmente completati a dicembre 2022. La suddivisione attuale delle riserve di Tether è evidenziata nel grafico sottostante:

Sfortunatamente, la necessità di fidarsi di entità centralizzate mantiene lo status quo e incatena l'industria crittografica a ciò da cui sta cercando di evolversi: la finanza tradizionale.

Le prossime due maggiori stablecoin collateralizzate in fiat per capitalizzazione di mercato sono USDC e BUSD. Entrambe hanno riserve contenenti principalmente titoli di stato statunitensi e un po' di fiat (<25%), e pubblicizzano che desiderano essere trasparenti con il loro collaterale.

Stablecoin Collateralizzate in Criptovaluta

Se un progetto crittografico è impegnato in DeFi, è logico che i fondatori di tale progetto vogliano evitare il sistema fiat e la centralizzazione. Per avere una stablecoin che si allontani completamente dal fiat (ma si basa ancora sul concetto di riserve), è possibile utilizzare un'altra criptovaluta come riserva. Il problema con questo modello è che le criptovalute hanno prezzi volatili, quindi il valore del collaterale immagazzinato nelle riserve può essere soggetto a fluttuazioni simili. L'unico modo per garantire che le riserve siano sufficienti contro un'azione di prezzo massiccia al ribasso sulla criptovaluta di riserva è sovra-collateralizzare la stablecoin, in modo che possa assorbire le significative fluttuazioni di prezzo del collaterale.

Un esempio di una stablecoin collateralizzata in criptovaluta è DAI, che è emessa dal progetto makerDAO su Ethereum. DAI è ancorata a USD e il suo valore è mantenuto attraverso posizioni di debito collateralizzate (CDP).

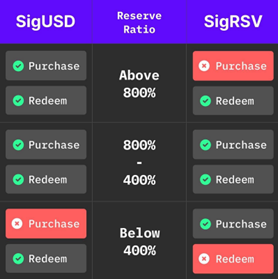

SigmaUSD è un esempio di un protocollo di emissione di stablecoin decentralizzato che utilizza riserve e non è collateralizzato da posizioni di debito.

Chiunque può coniare SigUSD così come SigRSV (per fornire riserva alla piattaforma). Questo protocollo consente alle persone di detenere USD supportati da Ergo e guadagnare commissioni bloccando il loro ERG come capitale di riserva. Il modello basato su riserve è superiore all'uso di posizioni di debito collateralizzate, poiché è in grado di prevenire liquidazioni a cascata durante una volatilità estrema degli asset collaterali.

Il protocollo utilizza un rapporto di riserva tra il 400% e l'800% per creare liquidità sana per acquirenti, venditori e detentori. Il rapporto di riserva è il valore di SigUSD in circolazione rispetto al valore dell'ERG immagazzinato nella riserva. Quindi, se 1000 SigUSD sono in circolazione e 1000 Erg valutati a 5 USD sono immagazzinati nelle riserve, allora il rapporto di riserva è del 500%.

Potresti chiederti, cosa significa mantenere il rapporto di riserva tra il 400% e l'800%? Se il rapporto di riserva è inferiore al 400%, allora il contratto impedisce agli utenti di riscattare SigRSV per l'ERG immagazzinato nella riserva. In questo modo, il protocollo può mantenere la parità tra USD e SigUSD. Inoltre, mentre il rapporto di riserva è sotto il 400%, gli utenti non saranno in grado di coniare SigUSD. Se il valore dell'ERG aumenta e porta il rapporto di riserva sopra il 400%, allora possono essere emessi più SigUSD. Allo stesso modo, se il valore dell'ERG diminuisce e il rapporto di riserva è sotto il 400%, allora la coniazione di SigUSD sarà bloccata.

Ciò significa che se qualcuno conia SigUSD per un valore di 100 dollari, allora ci saranno 400 dollari di SigRSV a sostegno. Questo lo rende equivalente a una posizione di debito collateralizzata al 75%. Il sistema protegge l'ancora di SigUSD a USD e previene i crolli improvvisi se il rapporto di riserva scende sotto il 400%.

I detentori di SigRSV beneficiano delle transazioni sul protocollo. Gli utenti che coniano o riscattano SigUSD pagano una commissione del 2,25%, che va ai detentori di riserva.

Stablecoin Non Collateralizzate

Le stablecoin non collateralizzate sono anche conosciute come stablecoin algoritmiche, in stile signoraggio o stablecoin supportate da crescita futura. Queste stablecoin non si basano su asset collaterali per mantenere il loro valore, ma utilizzano invece algoritmi matematici per controllare l'offerta della stablecoin per mantenere il suo valore stabile. Dexy è un esempio di una stablecoin in stile signoraggio.

Il protocollo Dexy utilizza ERG come riserva e Dexy come stablecoin. Ci sono due contratti che funzionano insieme: una banca e un DEX (CP-AMM). La banca detiene le riserve per il dispiegamento e conia nuovi Dexy nel DEX. Il DEX cerca di mantenere un prezzo oracle e ha funzioni di acquisto e vendita.

Il primo prodotto in fase di costruzione con il framework Dexy è DexyGold, dove il prezzo della stablecoin è ancorato al tasso USD/XAU v2 oracle pool. Dexy utilizza un meccanismo di ancoraggio unidirezionale, dove i token Dexy sono coniati da un contratto di emissione basato sul tasso dell'oracle pool e possono essere venduti su un Liquidity Pool (LP), simile a Uniswap V2. Per garantire la stabilità del protocollo, il riscatto dei token LP non è consentito quando il tasso dell'oracle pool è al di sotto di una certa percentuale del tasso LP.

Se il tasso dell'oracle pool è superiore al tasso LP, allora i trader possono arbitraggiare coniando token Dexy dalla scatola di emissione e vendendoli al LP. Se il tasso dell'oracle pool è inferiore al tasso LP, allora l'ERG raccolto nella scatola di emissione può essere utilizzato per riportare il tasso su un livello più alto eseguendo uno scambio.

Oltre le Stablecoin: Denaro Peer-to-Peer

ChainCash è un sistema monetario decentralizzato e peer-to-peer che mira a creare denaro collettivamente attraverso fiducia e asset blockchain. Affronta il problema dell'ineelasticità nell'offerta di asset blockchain, che può ostacolare il loro utilizzo nel mondo reale. Chaincash consente la creazione elastica di denaro in modo decentralizzato, mantenendo la qualità della valuta.

Gli utenti di ChainCash possono creare note di valori arbitrari, che possono o meno essere supportate da riserve in vari token digitali o asset del mondo reale. Queste note sono come rappresentazioni digitali di denaro che possono essere utilizzate per transazioni all'interno del sistema ChainCash. Per mantenere la qualità della valuta, l'accettazione di una nota dipende dal collaterale o dalla fiducia nell'emittente. Man mano che le note circolano, la loro qualità migliora generalmente grazie al collaterale collettivo e alla fiducia che le sostiene.

L'implementazione di ChainCash utilizzerà due contratti: uno per le note e uno per le riserve. Il sistema può tracciare diversi contratti di note e riserve, supportare vari predicati di accettazione e meccanismi di riscatto, e accogliere sistemi di valuta complementari, come i Sistemi di Scambio Locale (LETS) e le valute locali.

Mentre l'implementazione Layer Two è ancora in fase di considerazione, ChainCash offre un sistema monetario flessibile e decentralizzato che ha il potenziale di soddisfare diversi agenti economici a livello globale, affrontando le limitazioni degli asset blockchain tradizionali.

Conclusione

Le stablecoin sono una parte vitale dell'industria delle criptovalute perché fungono da ponte, integrando la finanza tradizionale con i nuovi sistemi crittografici basati su blockchain. Anche se il protocollo SigUSD è stato incredibilmente di successo, gli sviluppatori su Ergo continuano a innovare i potenziali design di una stablecoin crittografica. Attualmente, due importanti framework finanziari sono in fase di sviluppo: Dexy e ChainCash. Con lo sviluppo di ponti cross-chain (come Rosenbridge), le stablecoin di Ergo hanno il potenziale di offrire a molti altri utenti blockchain un deposito di valore sicuro e stabile - uno di cui l'industria ha disperatamente bisogno.

Share post

13 agosto 2025

9 luglio 2025

12 maggio 2025

7 agosto 2022